![]()

![]()

Housing Strengthening and CPI Softening

By Lyon Wealth Management on July 13, 2023

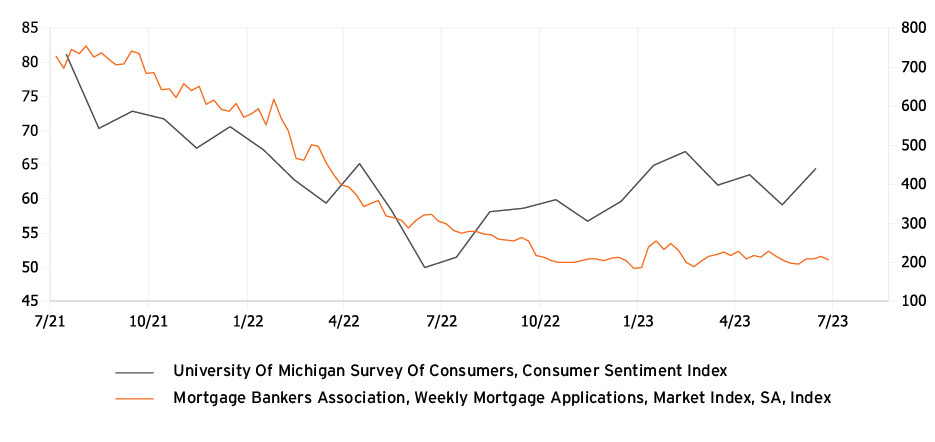

Consumer Confidence Reflected in Housing Market Activity

While homeowners are holding onto their low mortgage rates, new home buyers are absorbing higher interest rates, as mortgage applications have risen in 2023. In May, new home sales reached the highest level since February 2022 and housing starts reached the highest level since April 2022.

Positive housing activity corresponds to a pickup in consumer sentiment. 30-year fixed mortgage rates are averaging 8% – a combination of higher real income and low unemployment is adding to affordability, despite the higher rates. Confidence across home builders and home buyers has improved this year, and the traffic of prospective buyers of new homes has ticked up sharply this year.

Chart 1: Mortgage Applications Beginning to Follow Better Sentiment1

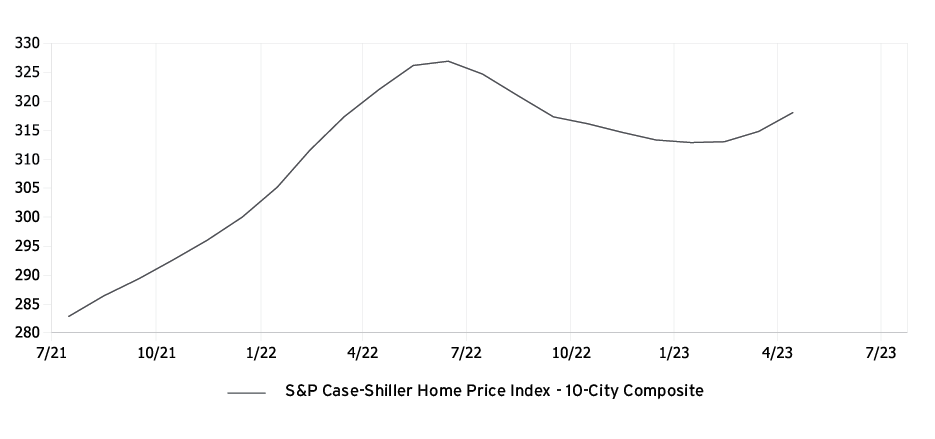

Limited housing inventory is also driving an upward swing in prices as demand picks back up. This reinforces confidence across home builders as we continue to see low vacancy rates and added traffic.

Chart 2: Home Prices Reversing Trend as Demand Gains Momentum2

The housing market is a major contributor toward broader economic growth, as home buyers also purchase goods and services as a part of home buying. The auto market is highly correlated with housing, and in the latest rail traffic data, automotive traffic increased +17% as dealerships re-stock to meet demand.

Housing Market’s Interest Rate Sensitivity … or Lack Thereof

The housing market tends to be one of the most interest-rate-sensitive sectors. Shortly after the Fed shifted its monetary policy, housing was really the first sector to feel the impact. Mortgage rates increased and demand fell sharply. Interestingly, despite rates continuing to move higher, the industry is rebounding strongly.

How can demand be picking up without rates coming down? Much of this effect has to do with the strong labor market. Higher real wages and increased consumer confidence are driving potential home buyers into the market. In addition, the U.S. is 5 million homes short in housing. There are now 5 million millennials who are first time buyers, which is also adding to the demand.

The Fed had previously hoped that a softer housing market would support its fight against inflation. The data indicates that housing market weakness has troughed. Further, the higher mortgage rates have reduced housing inventory – largely due to a drop in existing homes available on the market. There were 33% less existing homes available for sale in June 2023 than in February 2020.3

The latest inflation data continues to highlight housing as a contributor toward elevated inflation. While better housing activity may not slow inflation, it represents nearly 20% of U.S. GDP.

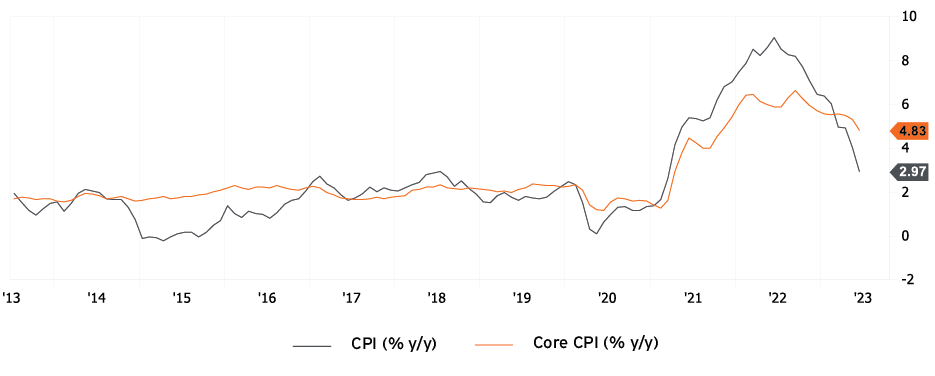

CPI Softer Than Expected

U.S. headline CPI cooled in June to 3% y/y, the slowest rate since March 2021. Core CPI also retreated to its slowest rate since November 2021, but remains elevated at 4.8% y/y.

Service sectors continue to drive inflation – shelter-related prices were the largest contributors to CPI in June. The housing rebound could add to persistent core inflation.

Fed Chair Jerome Powell has referenced his focus on core services, excluding housing, which decelerated to 4% y/y in June, although was little changed from the prior month.

Yields fell and stocks rallied on the CPI print. The next Fed FOMC meeting is July 26. We expect a 25 bps increase as Fed members remain hawkish and resound in their fight against inflation. The Fed’s CPI target is 2%. The trend is supportive that we are near the peak fed funds rate.

Chart 3: Annual Inflation Pace Retreating4

Subscribe to Our Newsletter!

Lyon Wealth Management is a group comprised of investment professionals registered with Hightower Advisors, LLC, an SEC registered investment adviser. Some investment professionals may also be registered with Hightower Securities, LLC (member FINRA and SIPC). Advisory services are offered through Hightower Advisors, LLC. Securities are offered through Hightower Securities, LLC.

This is not an offer to buy or sell securities, nor should anything contained herein be construed as a recommendation or advice of any kind. Consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. No investment process is free of risk, and there is no guarantee that any investment process or investment opportunities will be profitable or suitable for all investors. Past performance is neither indicative nor a guarantee of future results. You cannot invest directly in an index.

These materials were created for informational purposes only; the opinions and positions stated are those of the author(s) and are not necessarily the official opinion or position of Hightower Advisors, LLC or its affiliates (“Hightower”). Any examples used are for illustrative purposes only and based on generic assumptions. All data or other information referenced is from sources believed to be reliable but not independently verified. Information provided is as of the date referenced and is subject to change without notice. Hightower assumes no liability for any action made or taken in reliance on or relating in any way to this information. Hightower makes no representations or warranties, express or implied, as to the accuracy or completeness of the information, for statements or errors or omissions, or results obtained from the use of this information. References to any person, organization, or the inclusion of external hyperlinks does not constitute endorsement (or guarantee of accuracy or safety) by Hightower of any such person, organization or linked website or the information, products or services contained therein.

Click here for definitions of and disclosures specific to commonly used terms.

1550 Tiburon Blvd

Suite B Up #6

Tiburon, CA 94920

(415) 702-1622

Legal & Privacy

Web Accessibility Policy

Form Client Relationship Summary ("Form CRS") is a brief summary of the brokerage and advisor services we offer.

HTA Client Relationship Summary

HTS Client Relationship Summary

Hightower Advisors, LLC is a SEC registered investment adviser. Registration as an investment adviser does not imply a certain level of skill or training. Some investment professionals may also be registered with Hightower Securities, LLC and offer securities through Hightower Securities, LLC, member FINRA/SIPC. You can check the background of our firm and investment professionals on brokercheck.finra.org. Unless otherwise indicated relative to a specific award or ranking, Hightower Advisors, LLC does not pay a fee to be considered for any ranking or recognition, but may have paid to publicize rankings obtained and disseminated prior to 11.4.2022. All awards / rankings / ratings obtained and distributed on or after 11.4.2022 will be accompanied by specific disclosure as applicable.

© 2025 Hightower Advisors. All Rights Reserved.