![]()

![]()

Backstops and Buyouts

By Lyon Wealth Management on March 21, 2023

1. Bank Troubles in the Headlines, Well-Capitalized Institutions Providing Backstop. The systematically important financial institutions (SIFI) have over $400 billion in excess capital and well above the Basel III minimum 8% tier 1 capital ratio. Banks have complained about this regulatory oversight for the last 15 years, post-Great Financial Crisis. Now, they are in a much stronger position to support the government and the economy, while potentially benefitting from future upside, by offering backstop liquidity for struggling small and medium banks.

The government has established multiple programs in which financial institutions can access liquidity. There exists a “discount window” that offers loans for up to 90 days. The loans are typically less than the collateral put up by the bank, known as a “haircut,” which protects the Fed from unpaid loans and makes the lending vehicle beneficial for banks only in periods of stress. In 2008/2009 and 2020 the demand for discount window liquidity spiked. Last week, discount window demand surpassed both those periods and reached an all-time high.

The demand spiked, in part, due to the Fed removing the “haircut” from the loan and valuing the collateral at par. In addition, the Fed established a Bank Term Funding Program (BTFP), which similarly allowed banks to take out a loan valued at collateral’s face value. The BTFP offers loans for up to one year, as opposed to the 90-day loans available at the “discount window.”

In addition to these government lending facilities, big banks are stepping up to protect depositors and the broader economy from contagion. UBS purchased Credit Suisse over the weekend for $3.2 billion in an all-share deal.1 Eleven banks have pledged to deposit $30 billion into First Republic (FRC) to invoke confidence.2 It remains uncertain how markets absorb all the activity, but we’re observing first-hand the impact that tough regulation and well-capitalized SIFIs can have on economic stability. “This time is different” may just allude to bailouts under a different guise.

We are paying close attention to the daily action. This week, the Fed hosts its March FOMC meeting, uncertainty still surrounds the future of First Republic (after another credit downgrade), and U.S. lawmakers are considering raising the insurance on depositor accounts above the current $250,000 cap.3 Amid the uncertainty, we are actively managing our portfolios – focused on the fundamentals and anticipating future policy impacts.

2. UBS Buys Credit Suisse. The $3.2 billion all-share transaction, the result of a government-brokered deal, also includes significant liquidity provisions and Swiss government guarantees. Credit Suisse shareholders have experienced a 99% decline since the stock price’s peak in 2007. The deal also wipes out $17 billion in tier 1 (AT1) bonds that are now considered worthless, representing “the largest loss ever inflicted to AT1 investors since the birth of the asset class post-Global Financial Crisis.”4 U.S. bank stocks are higher in response to the weekend events.

3. Fed Policy. The Fed has raised rates 475 bps in the past year, and at this time last year the Fed was still purchasing bonds in the open market. The direct reason for raising rates has been to quell inflation and invoke price stability by slowing demand. Inflation has remained resilient and sticky; CPI remains +5.5% y/y and the Fed has continued to express a 2% target. Interest-sensitive sectors, like housing, felt the immediate impact from restrictive monetary policy. But consumer demand (e.g., travel and hospitality services), supply shortages (e.g., rents, autos) and broad pricing power have continued to drive sticky inflation.

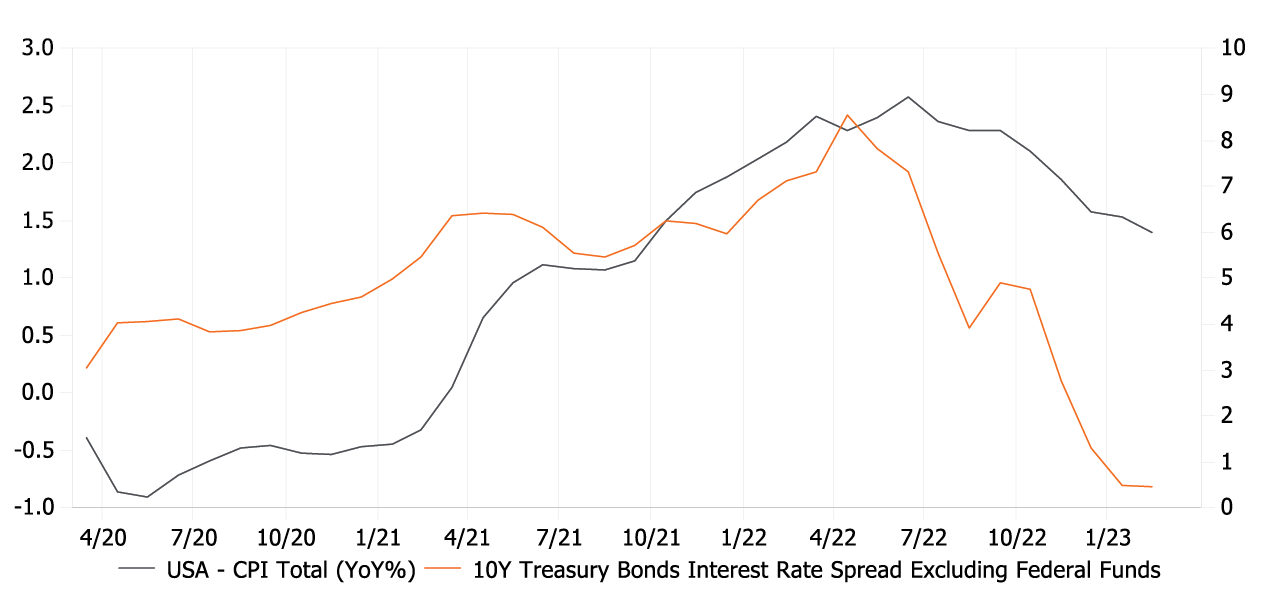

Chart 2: Negative Interest Rate Spread, Leading Indicator as Inflation Remains Elevated5

Now, the financial institutions are falling in line and will also become restrictive. In response to high rates and recent events, banks are likely to take risk off their balance sheets and restrict lending. Particularly small banks, which contribute 30% of total U.S. lending.

As banks implement their own restrictive lending programs, economic growth will likely slow. Apollo’s Torsten Slok estimates that tighter financial conditions plus tighter lending standards contribute to a 1.5% increase in the fed funds rate, in addition to the 475 bps hikes in the past year.

Last week, the European Central Bank (ECB) hiked 50 bps in the face of the impending Credit Suisse collapse. Whether the Fed decides to raise 25 bps, pause, or cut rates is uncertain, but markets are signaling that the Fed cannot continue to sustain higher rates. We think the Fed should pause, but they have made many mistakes and have a recent history of being late to act.

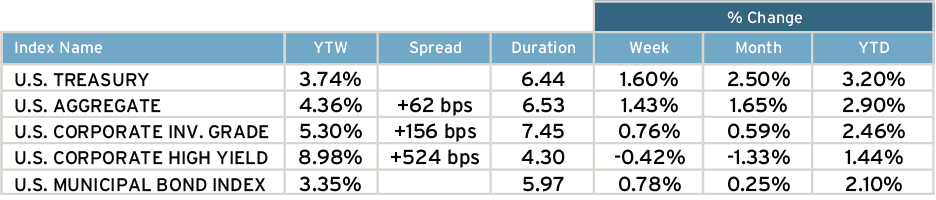

4. Credit Markets Pricing Lower Treasury Rates, Wider Credit Spreads. Volatility was the theme of last week’s market, visible in the Treasury Implied Volatility Index (MOVE Index) reaching 199 bps on Wednesday, the highest level since the 2009 GFC. The 2-year yield ended the week 13 bps lower, but fluctuated between 3.71% and 4.53%, the widest weekly range since September 2008. High Yield Spreads increased 65 bps to +542 bps, the fastest rise since September of 2022.

As of Friday’s close, markets are pricing in a 57% chance of a 25 bps hike at next week’s FOMC meeting. Investors will be keenly aware of Chairman Powell’s verbiage, given the fragility of the market.

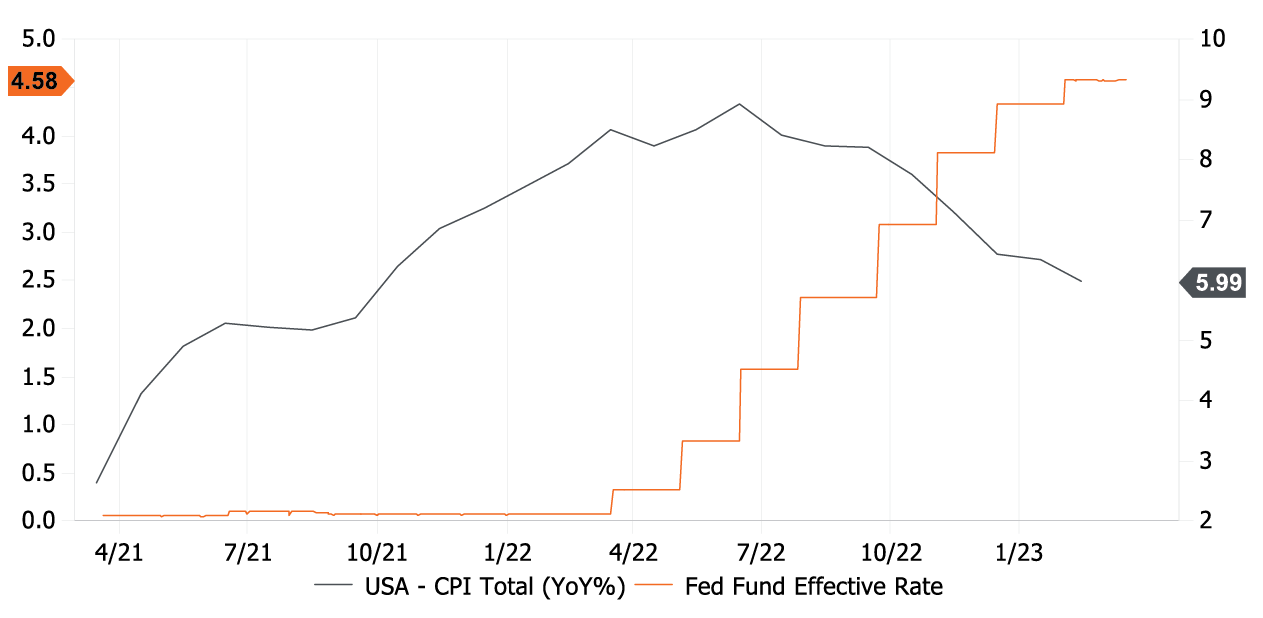

Chart 2: Inflation Remains Elevated Despite Historical Fed Rate Hike Regime6

5. Geopolitical Volatility, Because… of Course. China’s President Xi is set to visit Russia this week; both sides have communicated a shared interest in strengthening their relationship in regard to economic ties. China is walking a diplomatic tightrope.

Here at home, the U.S. government has continued to communicate threats towards banning TikTok. The parent company, ByteDance is a Chinese company accused of spying on U.S. citizens, stealing U.S. information and being a threat towards U.S. security. Last week, the White House endorsed the bipartisan RESTRICT act, which would allow broad power to regulate or ban technology produced by six countries: China, Cuba, Iran, North Korea, Russia and Venezuela.

6. The Week Ahead.

Earnings – Tuesday: NKE. Thursday: GIS, DRI.

Economics – Wednesday: FOMC Meeting. Thursday: Chicago Fed National Activity (February), Kansas City Fed Manufacturing (March). Friday: Durable Orders (February).

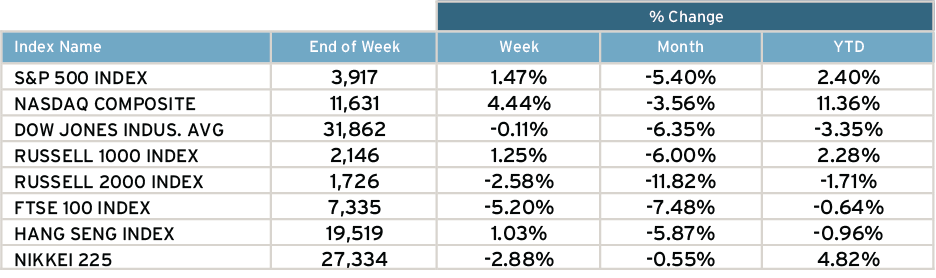

Return for Selected Indices7

Subscribe to Our Newsletter!

Lyon Wealth Management is a group comprised of investment professionals registered with Hightower Advisors, LLC, an SEC registered investment adviser. Some investment professionals may also be registered with Hightower Securities, LLC (member FINRA and SIPC). Advisory services are offered through Hightower Advisors, LLC. Securities are offered through Hightower Securities, LLC.

This is not an offer to buy or sell securities, nor should anything contained herein be construed as a recommendation or advice of any kind. Consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. No investment process is free of risk, and there is no guarantee that any investment process or investment opportunities will be profitable or suitable for all investors. Past performance is neither indicative nor a guarantee of future results. You cannot invest directly in an index.

These materials were created for informational purposes only; the opinions and positions stated are those of the author(s) and are not necessarily the official opinion or position of Hightower Advisors, LLC or its affiliates (“Hightower”). Any examples used are for illustrative purposes only and based on generic assumptions. All data or other information referenced is from sources believed to be reliable but not independently verified. Information provided is as of the date referenced and is subject to change without notice. Hightower assumes no liability for any action made or taken in reliance on or relating in any way to this information. Hightower makes no representations or warranties, express or implied, as to the accuracy or completeness of the information, for statements or errors or omissions, or results obtained from the use of this information. References to any person, organization, or the inclusion of external hyperlinks does not constitute endorsement (or guarantee of accuracy or safety) by Hightower of any such person, organization or linked website or the information, products or services contained therein.

Click here for definitions of and disclosures specific to commonly used terms.

1550 Tiburon Blvd

Suite B Up #6

Tiburon, CA 94920

(415) 702-1622

Legal & Privacy

Web Accessibility Policy

Form Client Relationship Summary ("Form CRS") is a brief summary of the brokerage and advisor services we offer.

HTA Client Relationship Summary

HTS Client Relationship Summary

Hightower Advisors, LLC is a SEC registered investment adviser. Registration as an investment adviser does not imply a certain level of skill or training. Some investment professionals may also be registered with Hightower Securities, LLC and offer securities through Hightower Securities, LLC, member FINRA/SIPC. You can check the background of our firm and investment professionals on brokercheck.finra.org. Unless otherwise indicated relative to a specific award or ranking, Hightower Advisors, LLC does not pay a fee to be considered for any ranking or recognition, but may have paid to publicize rankings obtained and disseminated prior to 11.4.2022. All awards / rankings / ratings obtained and distributed on or after 11.4.2022 will be accompanied by specific disclosure as applicable.

© 2025 Hightower Advisors. All Rights Reserved.