![]()

![]()

Special Edition: 46th Economic Symposium From Jackson Hole

By Lyon Wealth Management on August 28, 2023

Why Jackson Hole is Noteworthy

Every year, the Kansas City Fed hosts central bankers, policymakers, academics and economists from around the world at its annual economic policy symposium in Jackson Hole, Wyoming. This year’s event is titled, “Structural Shifts in the Global Economy.”

The attendees, which include Fed Chair Jerome Powell and other Fed members, release informative papers and participate in media interviews throughout the event in Jackson Hole, providing insight into future policy decisions and developments.

Bond Markets: Low Volatility, Rising Yields Ahead of Jackson Hole

Leading up to Jackson Hole, bond markets tend to be quiet as investors await signals from the event, however, weaker than expected PMI data caused a rally across the curve ahead of the speech.

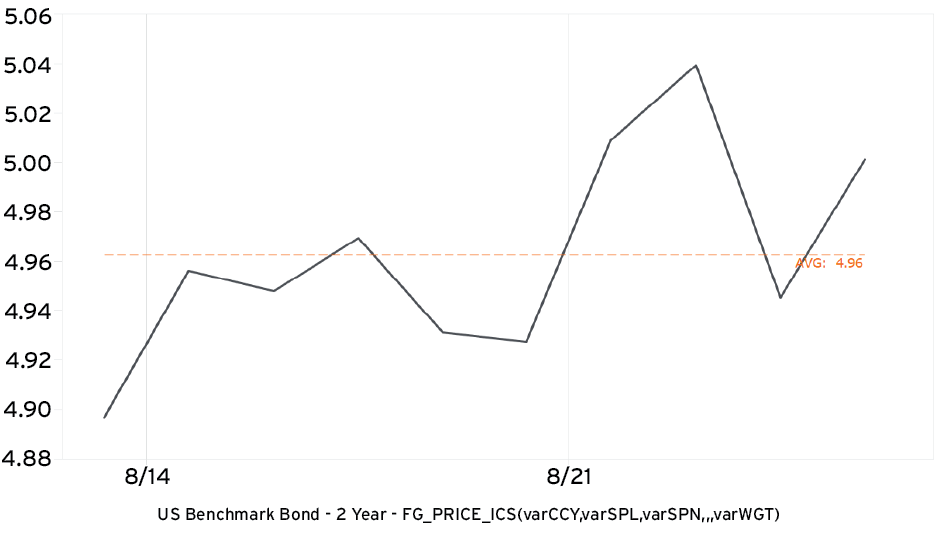

Chart 1: Two Year Treasury Yields1

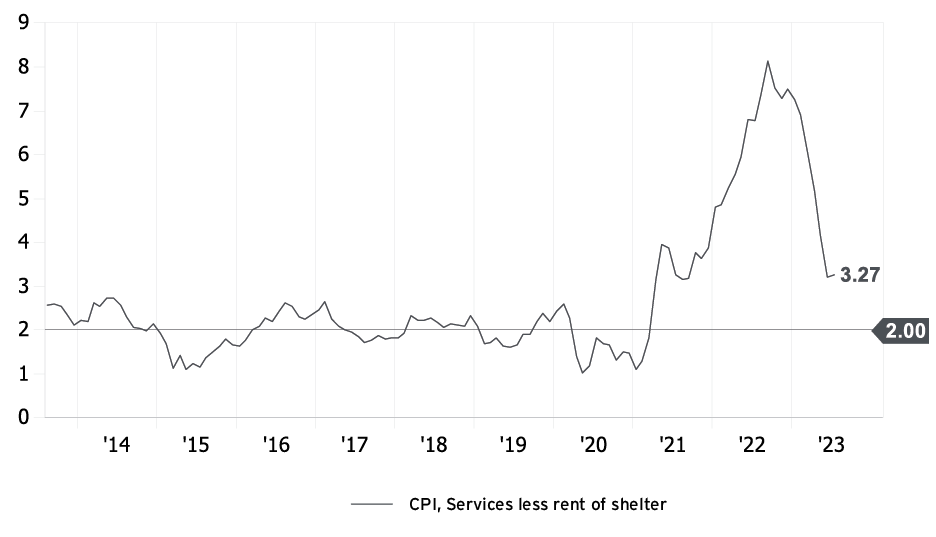

Powell held a hawkish tilt and remained consistent with the Fed’s 2% inflation target, remarking, “It is the Fed’s job to bring inflation down to our 2 percent goal, and we will do so.” This is indicative of further restrictive policy and a continuation of “higher for longer” rates while the Fed remains data-dependent. The Fed is focused on executing a soft landing by creating price stability without spiking default risk or causing economic activity to crater. The Fed maintains flexibility due to the consistently tight labor market, which supports the consumer, and continues to focus on key inflation datapoints like services, ex-housing.

While remaining steadfast in the fight toward 2% inflation, Powell noted favorable Core PCE readings in June and July reinforce the Fed’s confidence that inflation is moving down sustainably toward its goal. However, it remains unclear “the extent to which these lower readings will continue or where underlying inflation will settle over coming quarters.” Importantly, Core PCE data will be released next week. Expectations are for an acceleration to 4.2% from 4.1% in July.

Chart 2: Inflation Data Lower, Fed Looking for Sustainability of Trend Towards 2%2

This year it is a bit different in the bond market as bond yields have rallied due to the stronger economy, more supply from the Fed as it implements QT and Japan’s change in its monetary policies to end yield curve control. The 2-year Treasury yield has risen 65 bps YTD, 14 bps QTD and 131 bps off the March lows. Inflation has retreated, but sticky components remain as companies continue to implement pricing power strategies, an upside inflation risk. While the Fed is in its ninth inning of rate hikes, the yield curve is starting to anticipate a “higher for longer” scenario, and prices are reflecting a higher supply of Treasury securities.

Reaction to Jackson Hole and Updated Expectations

Policy decision making will continue to hinge on incoming data. The probability of a 25 bps hike by the November meeting jumped from 52% as of Thursday to 65% following Powell’s remarks. Further, the 2-year Treasury sold off, rising 3 bps, while the 10-year rose 1 bp during Powell’s speech.

Investment Solutions is a group comprised of investment professionals registered with Hightower Advisors, LLC, an SEC registered investment adviser. Some investment professionals may also be registered with Hightower Securities, LLC, member FINRA and SIPC. Advisory services are offered through Hightower Advisors, LLC. Securities are offered through Hightower Securities, LLC. This is not an offer to buy or sell securities. No investment process is free of risk, and there is no guarantee that the investment process or the investment opportunities referenced herein will be profitable. Past performance is neither indicative nor a guarantee of future results. The investment opportunities referenced herein may not be suitable for all investors. All data or other information referenced herein is from sources believed to be reliable. Any opinions, news, research, analyses, prices, or other data or information contained in this presentation is provided as general market commentary and does not constitute investment advice. Investment Solutions and Hightower Advisors, LLC or any of its affiliates make no representations or warranties express or implied as to the accuracy or completeness of the information or for statements or errors or omissions, or results obtained from the use of this information. Investment Solutions and Hightower Advisors, LLC assume no liability for any action made or taken in reliance on or relating in any way to this information. The information is provided as of the date referenced in the document. Such data and other information are subject to change without notice. This document was created for informational purposes only; the opinions expressed herein are solely those of the author(s) and do not represent those of Hightower Advisors, LLC, or any of its affiliates.

1Source: FactSet (chart). As of August 25, 2023.

2Source: FactSet (chart). As of August 23, 2023.

Subscribe to Our Newsletter!

Lyon Wealth Management is a group comprised of investment professionals registered with Hightower Advisors, LLC, an SEC registered investment adviser. Some investment professionals may also be registered with Hightower Securities, LLC (member FINRA and SIPC). Advisory services are offered through Hightower Advisors, LLC. Securities are offered through Hightower Securities, LLC.

This is not an offer to buy or sell securities, nor should anything contained herein be construed as a recommendation or advice of any kind. Consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. No investment process is free of risk, and there is no guarantee that any investment process or investment opportunities will be profitable or suitable for all investors. Past performance is neither indicative nor a guarantee of future results. You cannot invest directly in an index.

These materials were created for informational purposes only; the opinions and positions stated are those of the author(s) and are not necessarily the official opinion or position of Hightower Advisors, LLC or its affiliates (“Hightower”). Any examples used are for illustrative purposes only and based on generic assumptions. All data or other information referenced is from sources believed to be reliable but not independently verified. Information provided is as of the date referenced and is subject to change without notice. Hightower assumes no liability for any action made or taken in reliance on or relating in any way to this information. Hightower makes no representations or warranties, express or implied, as to the accuracy or completeness of the information, for statements or errors or omissions, or results obtained from the use of this information. References to any person, organization, or the inclusion of external hyperlinks does not constitute endorsement (or guarantee of accuracy or safety) by Hightower of any such person, organization or linked website or the information, products or services contained therein.

Click here for definitions of and disclosures specific to commonly used terms.

1550 Tiburon Blvd

Suite B Up #6

Tiburon, CA 94920

(415) 702-1622

Legal & Privacy

Web Accessibility Policy

Form Client Relationship Summary ("Form CRS") is a brief summary of the brokerage and advisor services we offer.

HTA Client Relationship Summary

HTS Client Relationship Summary

Hightower Advisors, LLC is a SEC registered investment adviser. Registration as an investment adviser does not imply a certain level of skill or training. Some investment professionals may also be registered with Hightower Securities, LLC and offer securities through Hightower Securities, LLC, member FINRA/SIPC. You can check the background of our firm and investment professionals on brokercheck.finra.org. Unless otherwise indicated relative to a specific award or ranking, Hightower Advisors, LLC does not pay a fee to be considered for any ranking or recognition, but may have paid to publicize rankings obtained and disseminated prior to 11.4.2022. All awards / rankings / ratings obtained and distributed on or after 11.4.2022 will be accompanied by specific disclosure as applicable.

© 2025 Hightower Advisors. All Rights Reserved.