![]()

![]()

Trick or Treat: A Week of Earnings and the Fed

By Lyon Wealth Management on November 1, 2022

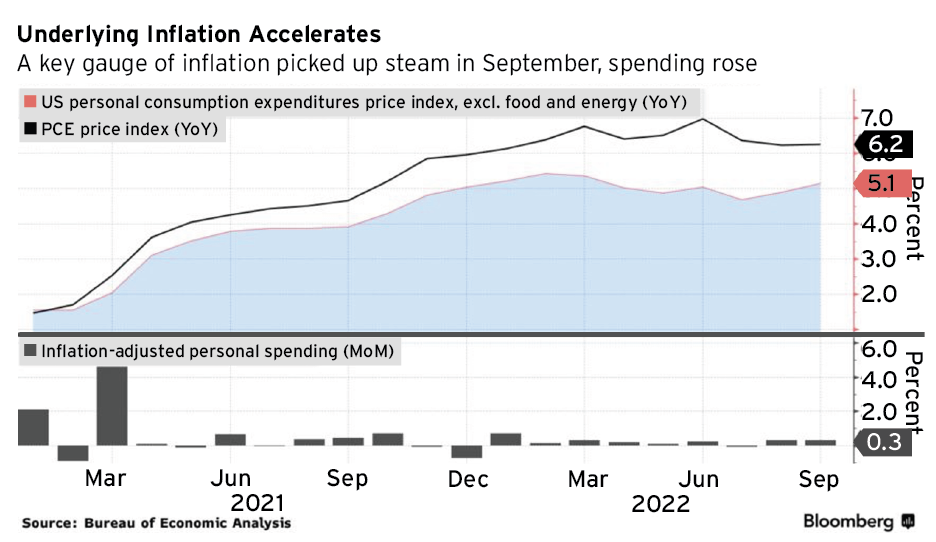

1. Macro Hot, Consumer Resilient. The Fed’s preferred measure for inflation, Core PCE, reported in-line with expectations and increased 0.5% m/m in September and 5.1% y/y. Consumer purchases of both goods and services remain stronger-than-expected, as spending increased in both categories. Importantly, personal spending grew more than expected, +0.6% m/m, as personal income increased +0.4% m/m.

Prices for services increased +0.6% m/m, led by housing and transportation services. Goods prices decreased -0.1% m/m, largely reflecting lower energy costs. Services represent approximately 80% of consumer spending, and both categories (goods and services) are much higher than last year. Prices for goods are +8.1% y/y, which includes food +11.9% and energy +20.3% y/y. Services are +5.3% y/y and continue to climb.

Chart 1: PCE and Core PCE Both Rise in September1

The Fed’s inflation target is 2% and currently, more than 83% of the CPI inflation basket is growing faster than 5% annualized.

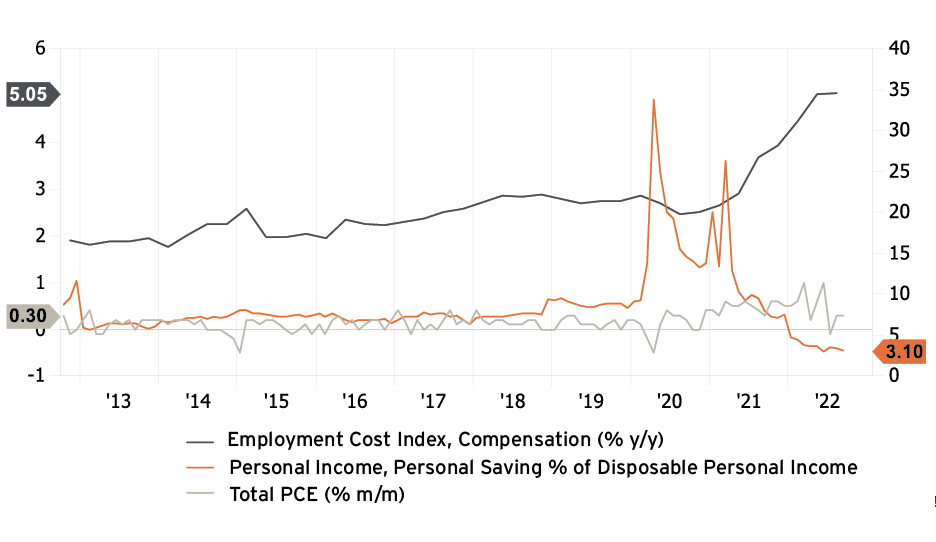

Consumer resilience is supporting economic stability, as the first preliminary Q3 GDP report indicated +2.6% q/q expansion. The consumer represents approximately 70% of U.S. GDP. Consumer resilience is also backed by growing employment costs – up +1.2% in Q3 and +5% y/y.

Higher employment costs reflect the rising cost pressures for businesses and tight labor market conditions. There are currently, still, 1.7 jobs per every available worker. While consumption has remained strong, the personal saving rate has fallen to 3.1% – the lowest rate since the great recession and a major reason why the Fed is determined to fight inflation, as the risks of persistent inflation outweigh negative impacts from higher rates and slowing growth.

Chart 2: Higher Wages, Less Saving, More Spending2

Stock markets have rallied off a number of factors, including oversold conditions, positive seasonal tailwinds, elevated inflation and solid growth. 70% of the S&P 500 has reported earnings, and 68% of the reporters have beaten earnings expectations. Value names have expanded EPS +8% y/y (led by the energy sector), while growth has contracted EPS -1.3% y/y.

2. Broad (Quiet) Participants in Stock Market Rally. The rally in equities is similar to the dynamic we experienced in July – following a steep sell-off and amid better-than-expected earnings. On Friday, 90% of stocks in the S&P 500 finished up on the day.

While news headlines remain focused toward growth and mega-cap tech, a number of quieter sectors, such as energy, industrials and financials, have produced encouraging results.

The notable laggards last week were concentrated in names like Meta (META), Amazon (AMZN), Alphabet (GOOGL) and Microsoft (MSFT) that disappointed on guidance and/or missed estimates. Meanwhile, names like Chevron (CVX), Exxon Mobil (XOM), Caterpillar (CAT), Honeywell (HON), Visa (V) and Haliburton (HAL) all reported encouraging results that reflect benefits from the long energy cycle, consumer spending, onshoring and capex spending themes. We suspect that energy inflation will remain elevated as the Fed remains hawkish. High prices within a traditionally cyclical commodity, even as consensus predicts a 2023 recession, are highly indicative that the energy supply challenges will be ongoing. The cash flows within the energy industry are historical, along with volumes.

The market appears to be embracing a new regime of outperformers. Energy, industrials and financials are the best performing sectors in October. These three sectors combined represent less than the entire technology sector within the S&P 500 and slightly more than the combined weights of the index’s top five positions: Apple (AAPL), Microsoft (MSFT), Amazon (AMZN), Tesla (TSLA) and Alphabet (GOOGL).

We’re hearing about layoffs and reduced hiring in select sectors, but labor overall remains very tight, and we receive an anticipated nonfarm payrolls and job openings report later this week. Hope for a Fed “pivot” has provided a balance to sentiment amid the high inflation and negative earnings revision fears. However, the tight labor market, persistent inflation and stable economic growth does not lead us toward participating in the “pivot” narrative. There are two important job data points out this week: JOLTs on Tuesday and Nonfarm Payrolls on Friday. We expect both to continue to show tightness in the labor market.

3. FOMC Meeting on Wednesday. Markets are pricing in a 75 bps rate November hike and, according to Bloomberg, there’s consensus for at least a 50 bps December hike, with 37% predicting a 75 bps December hike. We’ll listen, Wednesday, for any indication on what the December rate hike will be. Many sell-side economists have estimated a peak Fed funds rate around 5% next summer. Assuming the Fed hikes 75 bps on November 2, the new target rate will become 3.75-4.00%.

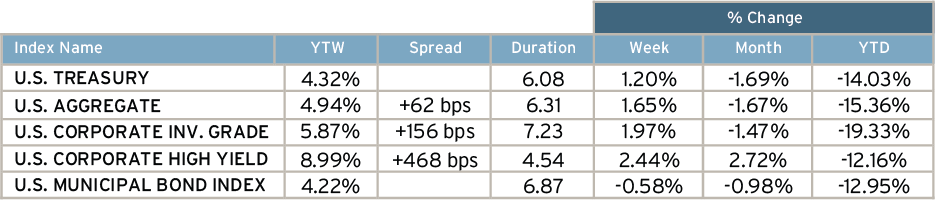

Bonds rallied through Thursday, then sold off a bit on Friday after stronger than anticipated economic data all but cemented another 75 bps hike at this week’s FOMC meeting. The 10-year yield ended the week 32 bps lower, while the two-year’s quick sell off on Friday left it down 9 bps. Municipal yields ended the week higher across the curve, with larger 9-11 bps moves seen on the long end. Investment Grade spreads remain elevated at +184 bps while High Yield spreads tightened 26 bps on Friday and have tightened 77 bps in the past month.

4. The Week Ahead.

Earnings – Tuesday: AFL, LLY, PFE, TAP, PSX, MCK, EA, AMD, MDLZ, CLX, CZR. Wednesday: CDW, MTCH, PARA, EMR, ROK, EL, QCOM, FTNT, EBAY, ETSY, MGM. Thursday: MAR, MRNA, ZTS, K, CMI, COP, EXPE, AMGN, PYPL. Friday: CTVA, CTRA, EOG, CAH, DUK, HSY.

Economics – Tuesday: ISM Manufacturing (October), JOLTs Job Openings (September). Wednesday: FOMC Meeting. Thursday: ISM Services (October), Unit Labor Costs and Productivity (Q3). Friday: Unemployment Rate and Nonfarm Payrolls (October)

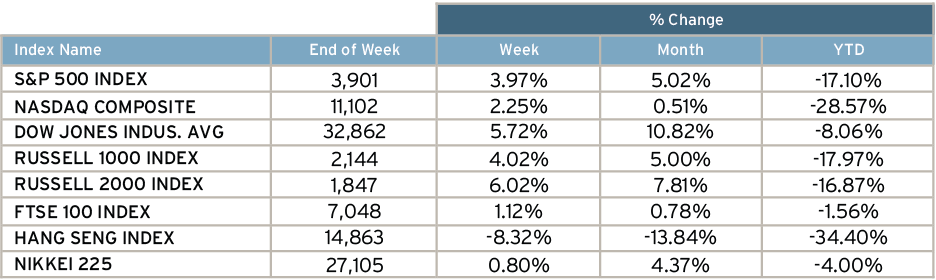

Return for Selected Indices3

Disclosure

Investment Solutions is a group comprised of investment professionals registered with Hightower Advisors, LLC, an SEC registered investment adviser. Some investment professionals may also be registered with Hightower Securities, LLC, member FINRA and SIPC. Advisory services are offered through Hightower Advisors, LLC. Securities are offered through Hightower Securities, LLC. This is not an offer to buy or sell securities. No investment process is free of risk, and there is no guarantee that the investment process or the investment opportunities referenced herein will be profitable. Past performance is neither indicative nor a guarantee of future results. The investment opportunities referenced herein may not be suitable for all investors. All data or other information referenced herein is from sources believed to be reliable. Any opinions, news, research, analyses, prices, or other data or information contained in this presentation is provided as general market commentary and does not constitute investment advice. Investment Solutions and Hightower Advisors, LLC or any of its affiliates make no representations or warranties express or implied as to the accuracy or completeness of the information or for statements or errors or omissions, or results obtained from the use of this information. Investment Solutions and Hightower Advisors, LLC assume no liability for any action made or taken in reliance on or relating in any way to this information. The information is provided as of the date referenced in the document. Such data and other information are subject to change without notice. This document was created for informational purposes only; the opinions expressed herein are solely those of the author(s) and do not represent those of Hightower Advisors, LLC, or any of its affiliates.

1Source: Bloomberg (chart) (October 31, 2022).

2Source: FactSet (chart) (October 31, 2022).

3Source: Bloomberg (October 31, 2022).

Subscribe to Our Newsletter!

Lyon Wealth Management is a group comprised of investment professionals registered with Hightower Advisors, LLC, an SEC registered investment adviser. Some investment professionals may also be registered with Hightower Securities, LLC (member FINRA and SIPC). Advisory services are offered through Hightower Advisors, LLC. Securities are offered through Hightower Securities, LLC.

This is not an offer to buy or sell securities, nor should anything contained herein be construed as a recommendation or advice of any kind. Consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. No investment process is free of risk, and there is no guarantee that any investment process or investment opportunities will be profitable or suitable for all investors. Past performance is neither indicative nor a guarantee of future results. You cannot invest directly in an index.

These materials were created for informational purposes only; the opinions and positions stated are those of the author(s) and are not necessarily the official opinion or position of Hightower Advisors, LLC or its affiliates (“Hightower”). Any examples used are for illustrative purposes only and based on generic assumptions. All data or other information referenced is from sources believed to be reliable but not independently verified. Information provided is as of the date referenced and is subject to change without notice. Hightower assumes no liability for any action made or taken in reliance on or relating in any way to this information. Hightower makes no representations or warranties, express or implied, as to the accuracy or completeness of the information, for statements or errors or omissions, or results obtained from the use of this information. References to any person, organization, or the inclusion of external hyperlinks does not constitute endorsement (or guarantee of accuracy or safety) by Hightower of any such person, organization or linked website or the information, products or services contained therein.

Click here for definitions of and disclosures specific to commonly used terms.

1550 Tiburon Blvd

Suite B Up #6

Tiburon, CA 94920

(415) 702-1622

Legal & Privacy

Web Accessibility Policy

Form Client Relationship Summary ("Form CRS") is a brief summary of the brokerage and advisor services we offer.

HTA Client Relationship Summary

HTS Client Relationship Summary

Hightower Advisors, LLC is a SEC registered investment adviser. Registration as an investment adviser does not imply a certain level of skill or training. Some investment professionals may also be registered with Hightower Securities, LLC and offer securities through Hightower Securities, LLC, member FINRA/SIPC. You can check the background of our firm and investment professionals on brokercheck.finra.org. Unless otherwise indicated relative to a specific award or ranking, Hightower Advisors, LLC does not pay a fee to be considered for any ranking or recognition, but may have paid to publicize rankings obtained and disseminated prior to 11.4.2022. All awards / rankings / ratings obtained and distributed on or after 11.4.2022 will be accompanied by specific disclosure as applicable.

© 2025 Hightower Advisors. All Rights Reserved.