![]()

![]()

Banks Tightening Might Ease the Fed

By Lyon Wealth Management on March 15, 2023

Recap of Events

Tuesday, March 7: Fed Chairman Jerome Powell testifies in front of congress. Amid disconcerting views from lawmakers on the Fed’s policy decisions, Chair Powell remained resolute that, “the ultimate level of interest rates is likely to be higher than previously anticipated.”1

Tuesday’s meeting indicated clearly that a hawkish 50 bps hike was back on the table for the Fed’s March 21-22 policy meeting. Investors priced in a 70.5% chance at day’s end, more than double the expectation from the prior day. The yield curve reached its deepest inversion since 1981.

Wednesday, March 8: After the markets closed, Silicon Valley Bank (SVB) announces it is issuing shares to generate liquidity. Shortly after, Moody’s downgraded the stock. This same day, Silvergate Capital (SI) announced it was shutting down after its crypto bet resulted in large losses.

Thursday, March 9: News breaks that U.S. regulators arrived at Silicon Valley Bank (SVB), investigating the impact of significant withdrawals. SVB stock tumbled more than 60% and it was clear there was an active run on the bank. During a conference call, Greg Becker, CEO of SVB urged customers to “stay calm” and “don’t panic.” Those comments proved disastrous.

The same day, Credit Suisse (CS) announced that it will delay its 2022 annual report after a late call from the U.S. SEC on Wednesday evening, indicating a need for further, “technical assessment.”

Friday, March 10: SVB fails. U.S. regulators took control of SVB, the nation’s 16th largest bank. Industry peers also experienced pressure on their deposits and sharp drops in share prices.

Sunday, March 12: A joint statement by the U.S. Treasury, Federal Reserve, and FDIC is released. The release indicated decisive action to protect SVB customers and Signature Bank customers, while closing both entities. Decisive action included, 1) making depositors whole, 2) invoking systemic rule and shutting down Signature Bank, and 3) creating a new liquidity facility enabling banks to access funds at par (not marked to market) to meet liquidity needs.

After Sunday, a total of three U.S. banks had failed within a matter of days.

Tuesday, March 14: Credit Suisse (CS) publishes its annual (delayed) report, which included that it had found “material weaknesses” in its financial reporting process for 2022 and 2021. The weaknesses included, “failure to design and maintain an effective risk assessment process.” The troubled bank has been plagued with “significantly higher withdrawals of deposits, non-renewal of maturing time deposits and net asset outflows,” since the second half of 2022.

Moody’s announced that it is changing its outlook on the U.S. banking system from stable to negative. Moody’s places six individual banks under review for downgrade.2

Wednesday, March 15: Amid significant volatility throughout the first half of the week, action escalates in European markets as Credit Suisse shares fall more than 20% and trading on the stock is halted. The collapse happened shortly after the chairman of the Saudi National Bank, Credit Suisse’s largest shareholder, said in an interview that it would not consider providing any more cash due to regulatory restrictions.

Credit Suisse CEO Urlich Koerner has sought to push back on the narrative, explaining that the bank’s liquidity basis is “very, very strong.”3

Restrictive Lending

Given the fluidity of the situation, it is widely expected that banks, particularly regional banks, will restrict lending programs as they seek to take risk off the table and secure liquidity. There continue to be reports that major banks are experiencing an influx of new depositors, which are leaving smaller, regional institutions.4 Some of the major banks being named as beneficiaries of new deposits include Bank of America (BAC) – which announced that it has received more than $15 billion in new deposits – plus JP Morgan (JPM), Citigroup (C) and Wells Fargo (WFC).5

Similarly, big banks are stepping in to help capitalize smaller banks that are under pressure with fleeing deposits. JP Morgan extended a credit facility to First Republic (FRC), which was under pressure, but said it had shored its finances with the additional funding.6 The situation changes by the minute, and there is clearly liquidity pressure on the less diversified, less regulated banks.

Reduced lending generates less revenue, particularly for less-diversified, smaller banks. In addition, slowing deposits also provide less liquidity. And ultimately, the steep rate hikes have produced major losses on long duration bonds being held on banks’ balance sheets – if banks are forced to sell (e.g., SVB) they will experience steep losses in those securities due to the move in interest rates.

Regional banks play a key role in the U.S. lending economy. Small banks account for 30% of all loans in the U.S. economy. As banks implement tighter lending standards due to high borrowing costs and credit risk, we anticipate economic growth to slow. The Fed has sought to slow the economy and implement restrictive policy, and it appears the banks are going to go along.

Volatility in Rate Expectations and Depleted Sentiment

Last Tuesday, markets predicted a 70-80% chance of the Fed raising rates 50 bps during next week’s FOMC meeting. Today, markets predict just a 45% chance for a 25 bps hike. Markets are anticipating the Fed to begin cutting rates by June and pricing in 100 bps of cuts by the end of the year.

These are incredible moves. A month ago, the December 2023 fed funds rate was pricing just above 5.5%. It is now 4.3% and the low was 3.75% earlier this week. A lower credit curve indicates that financial conditions are easing in the markets for potential approved borrowers.

Chart 1: Treasury Futures Prices Spike in the Past Week7

As rate hike expectations come down, inflation remains way too high and nowhere near the Fed’s 2% target. CPI was +6% y/y, Core CPI was +5.5% y/y, and Core CPI ex-shelter, which the Fed watches closely, remains +3.7% y/y. PPI commodity inflation data was cooler, but still +4.6% y/y. The consumer remains strong with revisions to retail sales better-than-expected. This puts the Fed in a quandary. We believe the Fed should not raise rates next week, but this has been a slow Fed, which has made many mistakes along the way.

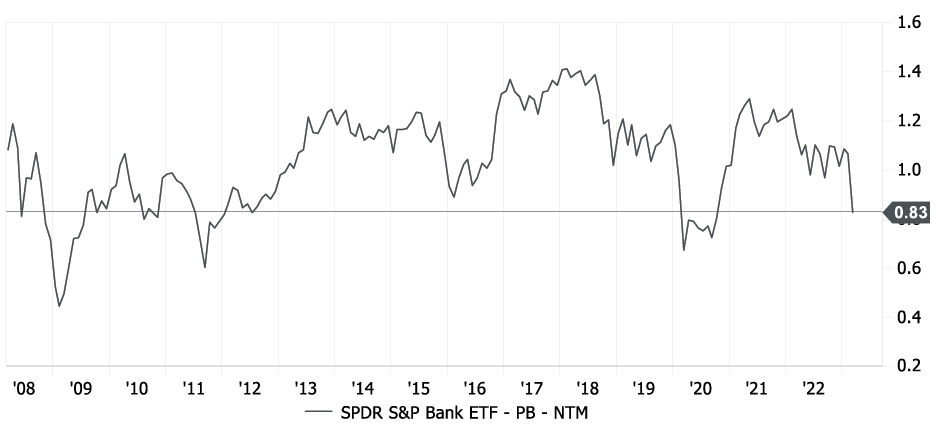

The Fear and Greed Index, which measures investor sentiment, is at “Extreme Fear” level. Similarly, stock valuations for banks continue to drop sharply, priced well-below book value and, excluding 2020, are at the lowest levels since 2012.

Chart 2: Banks Valued Sharply Lower8

Market volatility and depleted sentiment has created discount prices and opportunities, including with the major banks, which have enormous excess capital and are gaining share at the expense of the smaller regionals. Non-financials with strong balance sheets, free cash flows and excellent management teams are also being swept by the broader market volatility. These are times to be selectively investing for the long term.

Subscribe to Our Newsletter!

Lyon Wealth Management is a group comprised of investment professionals registered with Hightower Advisors, LLC, an SEC registered investment adviser. Some investment professionals may also be registered with Hightower Securities, LLC (member FINRA and SIPC). Advisory services are offered through Hightower Advisors, LLC. Securities are offered through Hightower Securities, LLC.

This is not an offer to buy or sell securities, nor should anything contained herein be construed as a recommendation or advice of any kind. Consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. No investment process is free of risk, and there is no guarantee that any investment process or investment opportunities will be profitable or suitable for all investors. Past performance is neither indicative nor a guarantee of future results. You cannot invest directly in an index.

These materials were created for informational purposes only; the opinions and positions stated are those of the author(s) and are not necessarily the official opinion or position of Hightower Advisors, LLC or its affiliates (“Hightower”). Any examples used are for illustrative purposes only and based on generic assumptions. All data or other information referenced is from sources believed to be reliable but not independently verified. Information provided is as of the date referenced and is subject to change without notice. Hightower assumes no liability for any action made or taken in reliance on or relating in any way to this information. Hightower makes no representations or warranties, express or implied, as to the accuracy or completeness of the information, for statements or errors or omissions, or results obtained from the use of this information. References to any person, organization, or the inclusion of external hyperlinks does not constitute endorsement (or guarantee of accuracy or safety) by Hightower of any such person, organization or linked website or the information, products or services contained therein.

Click here for definitions of and disclosures specific to commonly used terms.

1550 Tiburon Blvd

Suite B Up #6

Tiburon, CA 94920

(415) 702-1622

Legal & Privacy

Web Accessibility Policy

Form Client Relationship Summary ("Form CRS") is a brief summary of the brokerage and advisor services we offer.

HTA Client Relationship Summary

HTS Client Relationship Summary

Hightower Advisors, LLC is a SEC registered investment adviser. Registration as an investment adviser does not imply a certain level of skill or training. Some investment professionals may also be registered with Hightower Securities, LLC and offer securities through Hightower Securities, LLC, member FINRA/SIPC. You can check the background of our firm and investment professionals on brokercheck.finra.org. Unless otherwise indicated relative to a specific award or ranking, Hightower Advisors, LLC does not pay a fee to be considered for any ranking or recognition, but may have paid to publicize rankings obtained and disseminated prior to 11.4.2022. All awards / rankings / ratings obtained and distributed on or after 11.4.2022 will be accompanied by specific disclosure as applicable.

© 2025 Hightower Advisors. All Rights Reserved.