![]()

![]()

China Chronicles: Learnings so Far This Earnings Season

By Lyon Wealth Management on August 3, 2023

Top-Down vs. Bottom-Up Approach to China

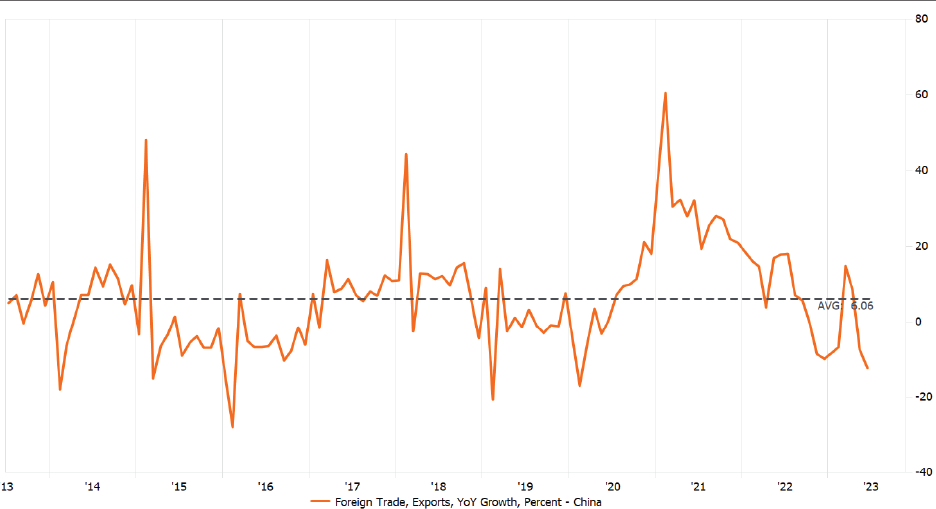

China has long been one of the driving forces in the global economy. While China-U.S. relations have steadily deteriorated since the Trump tariffs in 2018, China continues to dominate global trade, increasing its share of global good exports to 14.4% in 2022 from 13% in the prior year.1 China has long benefited from strong consumer spending overseas. However, Covid lockdowns, rising global interest rates, geopolitical tensions and reshoring present challenges. While hope abounded in early 2023 as China removed pandemic-era restrictions, that hope has plateaued as export numbers and global discretionary spending on goods has waned in the face of a possible recession.

As economic data steadily improves in the U.S., mixed economic data out of China tells a different story. The benefit of corporate earnings season is that we get to hear directly from the companies that operate on the ground in places like China. As earnings season kicks into high gear, we see it prudent to recap what has been reported by a broad array of companies, offering a bottom-up analysis on China.

Chart 1: China Exports, y/y Growth2

Macro Data Mixed

China’s economic data is a mixed bag. Caixin Manufacturing PMI, which is a survey that measures China’s manufacturing activity, recently dipped into contractionary territory (49.2) after two consecutive months of expansion. However, Caixin Services PMI, which measures China’s services activity, remains in expansionary territory (53.9), albeit at the lowest point since January.

There are underlying factors limiting China’s ability to return to pre-pandemic levels. First, leading-edge semiconductor export restrictions on U.S. companies to China enacted last fall in the name of national security have curtailed China’s ability to reinvigorate its economy. Further, at the onset of the pandemic, U.S. and Chinese governments restricted flights to prevent the spread of the disease. There were about 350 flights a week between the two countries prior to the pandemic; currently, that number sits at 24. The lacking ability to travel has put a ceiling on travel expenditures.

Consumer Facing Commentary Signals Continued Growth

Many tourism-related companies, including airlines, hotels and leisure, have reported a strong rebound in consumption. Most recently, Marriott International (MAR) reported that average daily room rate increased 34% y/y, along with occupancy up 28% y/y, which drove the company to raise its full-year earnings outlook.3 On Boeing’s (BA) recent earnings call, management noted that “the return to service in China is now largely complete.” Driving the China recovery is passenger traffic at 87% of pre-pandemic levels and domestic travel up 300% y/y, indicating Chinese consumers are looking to get back out and spend. United Airlines (UAL) had similar positive commentary on China, as it reported international margins well-above 2019 levels, with a 27% increase for international capacity.4 United anticipates expanding its international offerings later this year after finalizing the largest widebody aircraft order in history with Boeing.

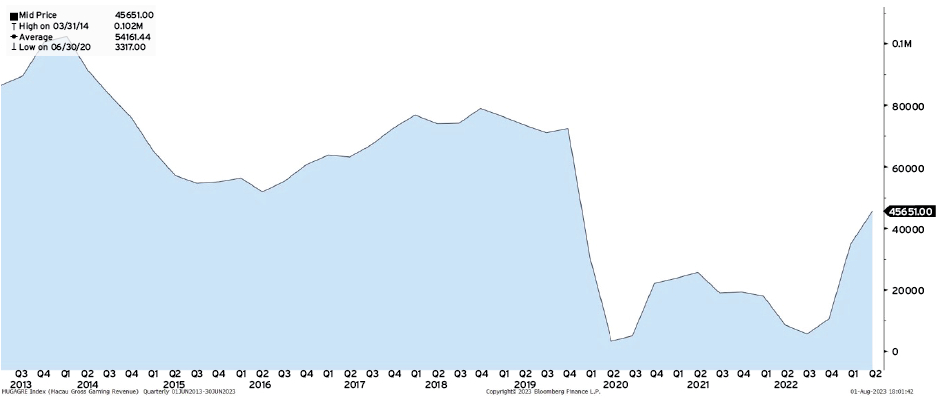

While it is evident that Chinese consumers are back to spending domestically, Chinese companies are looking to regain their footing in international markets as well. This was noted by Meta (META) during its recent second quarter earnings call. Advertising revenue growth was bolstered by the online commerce vertical, which was driven by strong spend among advertisers in China looking to reach customers in other markets.5 Meta credits easing regulations on the Chinese gaming industry in tandem with improved artificial intelligence advertising targeting. Shown in the chart below, Macau, China’s version of Las Vegas, has seen a recent resurgence in revenues.

Chart 2: Macau Gaming Revenue6

Evidently, China’s consumer-facing industries are gaining momentum. However, industrial, energy, materials and even semiconductor companies will offer a lens into the plumbing of the Chinese economy.

It Works! Materials, Energy and Semiconductor Strength

Chemical production, more specifically plastic, is a good place to start. China is the world’s largest consumer of plastics including high-density polyethylene (HDPE).7 Dow Chemical (DOW) is a major manufacturer of HDPE and other petrochemical products. Key end markets for Dow’s chemical products include construction, industrial, mobility and personal care products.8 While yet to fully materialize, Dow noted its ability to “move good volume into China.”9 Management is optimistic their efforts will result in further China growth, and acknowledged that despite lower than pre-pandemic levels, GDP growth in the 4.5-5% range is still very good for the second largest economy in the world.10 Exxon Mobile (XOM), like Dow, has business in petrochemicals, and furthered the positive commentary in its recent earnings call where management noted a recent increase in chemicals demand.11 Exxon’s second quarter chemical sales increased sequentially and said that the demand of out China looks reasonable, however, it may take a few months for demand to catch up with current supply.

China is the world’s second largest consumer of crude oil.12 Goldman Sachs recently downgraded China’s 2023 crude oil demand by 125kb/d but noted a recovery in jet fuel demand provides potential upside for the projection.13 Previously mentioned commentary out of both Boeing and United Airlines provides evidence that jet fuel demand in China is set to accelerate.

China is the world’s largest consumer of refined copper, a key input in electrification, including the quickly growing electric vehicles segment.14 Freeport-McMoRan (FCX) is a major player in copper mining. It weighed in on China during its most recent earnings call, confirming demand for copper in China is strong and that the country remains the world’s largest copper consumer.15 While acknowledging the slower recovery from the era of Covid lockdowns, copper consumption continues to grow, supported by investments in electrical grid and EV production.16 Despite the slower than expected recovery, the electrification theme remains a bright spot. China is one of the largest consumers of commodities given its manufacturing capacity and massive population. With a large population, healthcare providers have large interests in the nation.

China’s medical device market is valued at $42.6 billion or 8.3%, putting it in the top 10 markets globally.17 GE Healthcare (GEHC) is a major producer of medical devices that are consumed by China.18 GE Healthcare was able to grow sales within all regions including China, where revenue grew double digits. The company predicts that this growth should continue into the third quarter and is increasing its China localization.19 The medical device manufacturer’s commentary is in line with the commodity driven companies previously mentioned. Key components in medical as well as almost every other device are semiconductors.

As previously noted, the United States Bureau of Industry and Security (BIS) announced export controls on high-end semiconductor devices to limit China’s potential military and supercomputer capabilities. Despite these export controls, Lam Research (LRCX) noted in its recent fiscal fourth quarter earnings call that demand from Chinese customers has shifted toward trailing edge chips where they are permitted to invest.20 These chips are used in typical household products and handheld devices. The increased wafer fabrication equipment (WFE) expenditure out of China allowed Lam to increase its expectation for global WFE expenditures. Investors see the expenditures out of China as a bridge to a broader increase in WFE that is expected in the coming months.

Primed for a Recovery

The pandemic, rapidly changing technology and a power struggle with the U.S. have all worked against China in recent years. However, American management teams’ willingness to work with their Chinese counterparts is displayed in the earnings call commentary. The broad-based commentary from the earnings calls gives the impression that China is a far cry from submitting and will continually find new avenues for growth. For that reason, we remain confident in companies with China exposure and continue to keep a close eye on all data that is released, for we will be positioned to capitalize on the opportunity when it presents itself.

Subscribe to Our Newsletter!

Lyon Wealth Management is a group comprised of investment professionals registered with Hightower Advisors, LLC, an SEC registered investment adviser. Some investment professionals may also be registered with Hightower Securities, LLC (member FINRA and SIPC). Advisory services are offered through Hightower Advisors, LLC. Securities are offered through Hightower Securities, LLC.

This is not an offer to buy or sell securities, nor should anything contained herein be construed as a recommendation or advice of any kind. Consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. No investment process is free of risk, and there is no guarantee that any investment process or investment opportunities will be profitable or suitable for all investors. Past performance is neither indicative nor a guarantee of future results. You cannot invest directly in an index.

These materials were created for informational purposes only; the opinions and positions stated are those of the author(s) and are not necessarily the official opinion or position of Hightower Advisors, LLC or its affiliates (“Hightower”). Any examples used are for illustrative purposes only and based on generic assumptions. All data or other information referenced is from sources believed to be reliable but not independently verified. Information provided is as of the date referenced and is subject to change without notice. Hightower assumes no liability for any action made or taken in reliance on or relating in any way to this information. Hightower makes no representations or warranties, express or implied, as to the accuracy or completeness of the information, for statements or errors or omissions, or results obtained from the use of this information. References to any person, organization, or the inclusion of external hyperlinks does not constitute endorsement (or guarantee of accuracy or safety) by Hightower of any such person, organization or linked website or the information, products or services contained therein.

Click here for definitions of and disclosures specific to commonly used terms.

1550 Tiburon Blvd

Suite B Up #6

Tiburon, CA 94920

(415) 702-1622

Legal & Privacy

Web Accessibility Policy

Form Client Relationship Summary ("Form CRS") is a brief summary of the brokerage and advisor services we offer.

HTA Client Relationship Summary

HTS Client Relationship Summary

Hightower Advisors, LLC is a SEC registered investment adviser. Registration as an investment adviser does not imply a certain level of skill or training. Some investment professionals may also be registered with Hightower Securities, LLC and offer securities through Hightower Securities, LLC, member FINRA/SIPC. You can check the background of our firm and investment professionals on brokercheck.finra.org. Unless otherwise indicated relative to a specific award or ranking, Hightower Advisors, LLC does not pay a fee to be considered for any ranking or recognition, but may have paid to publicize rankings obtained and disseminated prior to 11.4.2022. All awards / rankings / ratings obtained and distributed on or after 11.4.2022 will be accompanied by specific disclosure as applicable.

© 2025 Hightower Advisors. All Rights Reserved.