![]()

![]()

Jamie Dimon’s Annual Letter to Shareholders

By Lyon Wealth Management on April 6, 2023

Annual Letter

This week, Jamie Dimon, chairman and CEO of JP Morgan Chase released an annual letter to shareholders that included perspective on JP Morgan and the banking sector more broadly, along with his opinion on the current state of economic and government affairs. Many might remember nearly a year ago, Dimon told a group of investors that a “hurricane” was coming for the economy. Dimon offered balanced remarks, noting significant risks and uncertainties, long-term opportunities and frustrations.

Dimon, as CEO of the world’s largest bank, has significant power and, importantly, insights provided by his unique access to global markets and global leaders. Therefore, we find that it is often worth paying attention to what he has to say.

The full letter can be found here and some key takeaways are summarized below.

State of the Banks: Regulated, Capitalized, and Critical to Global Economies

Dimon mentioned the company’s resilience, which many CEOs have similarly emphasized throughout the past few years. JP Morgan “grew market share in several of their businesses and continued to make significant investments in products, people and technology while exercising strict credit discipline.” It is worthwhile emphasizing that credit discipline has been a theme since far before the recent banking turmoil – banks have implemented higher credit standards throughout recent quarters.

Dimon emphasized the risks “hiding in plain sight” within the U.S. banking system, created by the “rapid deterioration in fair value of held-to-maturity portfolios” and “lack of stickiness of certain uninsured deposits.” Dimon believes that “repercussions” will be felt “for years to come” and the crisis damages all banks. “While the Fed’s balance sheet has come down by approximately $550 billion, deposits at the banks have come down by $1 trillion, largely uninsured deposits.”

Midsized, regional and community banks have a vital role to play within the economy, as do complex, large banks. Banks play a vital role across global economies and within small communities, and effective regulation supports the industry’s health, competitiveness and client confidence. Most businesses, including banks, play a critical role in being there for their clients and it is important that this continues.

Consumer Strength, Fiscal Deficit and Monetary Tightening

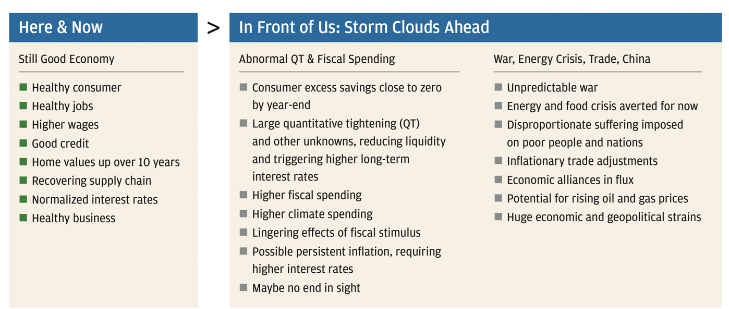

While the global economy “marched ahead,” 2022 was “not normal, economically speaking.” Dimon listed several extreme events, including the Russia-Ukraine war, 40-year high inflation, 425 bps increase in the fed funds rate, stock markets -20%, and 50-year low unemployment.

The consumer, which represents 65% of the U.S. economy, continues to drive growth. Consumers in 2022 spent 7-9% more than in the prior year and 23% more than pre-COVID. Balance sheets are in great shape, with $1.2 trillion more “excess cash” in their checking accounts than pre-COVID. Low unemployment, higher wages (particularly at the low end) and 10 years of home appreciation are supporting consumers. For businesses, supply chains are recovering, and credit losses are extremely low.

There is ample weakness too, but it “should not be considered […] anything like what we experienced in 2008.”

Yield curve inversion, particularly looking at longer-term rates, reflects views on risk and safety. The recent bank failures have provoked jitters and increased odds of recession, but “it is unclear whether this disruption is likely to slow consumer spending.” Dimon goes on to say that “by sometime late this year or early next year, we expect consumers will have spent the bulk of their remaining excess savings.”

Fed policy manipulation and fiscal deficit is magnifying inflation and potential instability. “This may be a once-in-a-generation sea change.” Governments around the world need to service higher debt-to-GDP ratios as QE policy shifts to QT. The U.S. fiscal deficit is “estimated to be $1.4-1.8 trillion per year” for the next three years before any costs related to future recessions, war or other unforeseeable events.

U.S. Requires Changes to Maintain Effective Global Leadership

The Inflation Reduction Act (IRA) combined with the CHIPS Act and Bipartisan Infrastructure Law “will create huge opportunities for companies, investors and entrepreneurs across virtually every industry group.” These bills, if implemented effectively, will support diversifying supply chains to be more resilient, securing national interests and promoting GDP growth. While inflation and interest rates are uncertain, Dimon is more concerned about geopolitical and critical infrastructure risks.

Dimon believes we must create a comprehensive global economic strategy that focuses on four pillars: a U.S. GDP growth strategy, an industrial policy that drives GDP and national security, fixing income inequality, and the U.S. taking a leadership role in a global economic strategy.

A Balanced Conclusion

It is no longer rainbows and sunshine, but it is no hurricane either. It is both pockets of strength and weakness, and possibly a macro-overhang that will drive markets and economic growth for the next number of years. There are reasons for optimism that the U.S. is resilient with healthy consumers, complex capital markets and fiscal stimulus that can continue to drive economic growth. Unfortunately, there too remains uncertainties like inflation and geopolitical risks. Banks are well-capitalized, stress-tested and prepared for the tail risks.

Subscribe to Our Newsletter!

Lyon Wealth Management is a group comprised of investment professionals registered with Hightower Advisors, LLC, an SEC registered investment adviser. Some investment professionals may also be registered with Hightower Securities, LLC (member FINRA and SIPC). Advisory services are offered through Hightower Advisors, LLC. Securities are offered through Hightower Securities, LLC.

This is not an offer to buy or sell securities, nor should anything contained herein be construed as a recommendation or advice of any kind. Consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. No investment process is free of risk, and there is no guarantee that any investment process or investment opportunities will be profitable or suitable for all investors. Past performance is neither indicative nor a guarantee of future results. You cannot invest directly in an index.

These materials were created for informational purposes only; the opinions and positions stated are those of the author(s) and are not necessarily the official opinion or position of Hightower Advisors, LLC or its affiliates (“Hightower”). Any examples used are for illustrative purposes only and based on generic assumptions. All data or other information referenced is from sources believed to be reliable but not independently verified. Information provided is as of the date referenced and is subject to change without notice. Hightower assumes no liability for any action made or taken in reliance on or relating in any way to this information. Hightower makes no representations or warranties, express or implied, as to the accuracy or completeness of the information, for statements or errors or omissions, or results obtained from the use of this information. References to any person, organization, or the inclusion of external hyperlinks does not constitute endorsement (or guarantee of accuracy or safety) by Hightower of any such person, organization or linked website or the information, products or services contained therein.

Click here for definitions of and disclosures specific to commonly used terms.

1550 Tiburon Blvd

Suite B Up #6

Tiburon, CA 94920

(415) 702-1622

Legal & Privacy

Web Accessibility Policy

Form Client Relationship Summary ("Form CRS") is a brief summary of the brokerage and advisor services we offer.

HTA Client Relationship Summary

HTS Client Relationship Summary

Hightower Advisors, LLC is a SEC registered investment adviser. Registration as an investment adviser does not imply a certain level of skill or training. Some investment professionals may also be registered with Hightower Securities, LLC and offer securities through Hightower Securities, LLC, member FINRA/SIPC. You can check the background of our firm and investment professionals on brokercheck.finra.org. Unless otherwise indicated relative to a specific award or ranking, Hightower Advisors, LLC does not pay a fee to be considered for any ranking or recognition, but may have paid to publicize rankings obtained and disseminated prior to 11.4.2022. All awards / rankings / ratings obtained and distributed on or after 11.4.2022 will be accompanied by specific disclosure as applicable.

© 2025 Hightower Advisors. All Rights Reserved.